FOR IMMEDIATE RELEASE

Contact: J. Craig Shearman

(202) 257-3678 craig@shearmancommunications.com

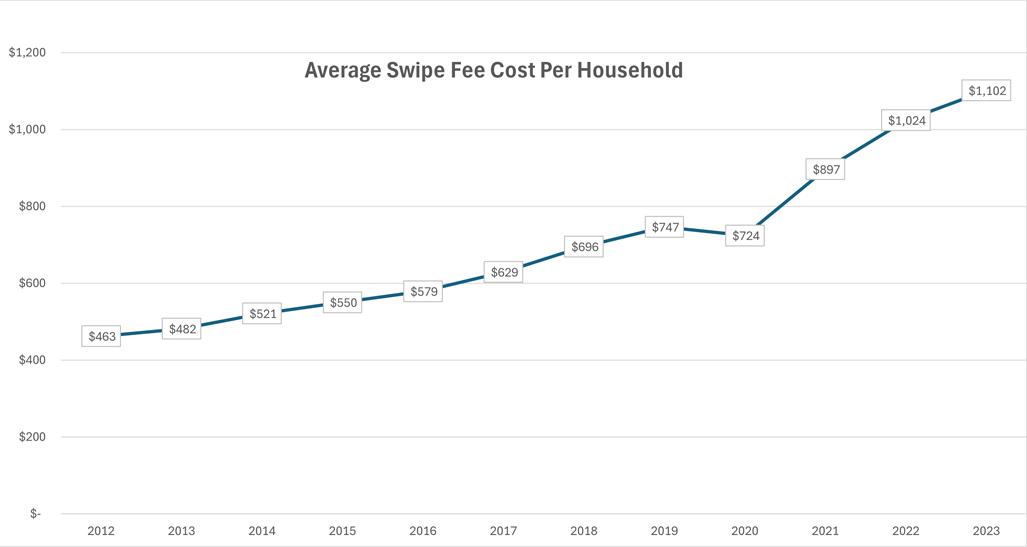

WASHINGTON, April 25, 2024 – Soaring credit and debit card swipe fees cost the average U.S. household more than $1,100 last year, the Merchants Payments Coalition said today.

“American families should not get bilked for more than $1,100 each year on swipe fees,” MPC Executive Committee member and National Retail Federation Senior Director of Government Relations Dylan Jeon said. “It’s time for the card industry to stop gouging American consumers and small businesses and compete to offer market-based, competitive fees. Instead, the credit card industry uses cartel pricing to extract more and more dollars from Americans’ pockets each year. Congress needs to pass the Credit Card Competition Act to fix the broken credit card market.”

Credit and debit card swipe fees rose to a record $172.05 billion in 2023, according to numbers released in March by the Nilson Report. That works out to $1,102 for the average household, up from $1,024 in 2022, when swipe fees totaled $160.7 billion, according to MPC estimates. Swipe fees amounted to $897 for the average household in 2021 and $724 in 2020. The fees have more than doubled over the past decade and are up 50 percent since the pandemic.

Source: Merchants Payments Coalition

Last year’s total included $100.8 billion in swipe fees for Visa and Mastercard credit cards alone, which account for more than 80 percent of the market. That was up from $93.2 billion in 2022 and marked the first time the figure topped the $100 billion mark. Swipe fees contribute significantly to net profit margins of 53 percent at Visa, 43 percent at Mastercard and 45 percent at JPMorgan Chase, the largest issuer of credit cards under their brands, according to the most recent quarterly earnings reports for the companies. By contrast, net profit for general retail averages only 3 percent.

Under a proposed settlement of a long-running class-action lawsuit, Visa and Mastercard have agreed to temporarily lower credit card swipe fees by four basis points (0.04 percentage point) for specific transactions and seven basis points on average. But the settlement applies only to the banks’ portion of swipe fees, and Mastercard is already increasing a key network fee, costing merchants an estimated $259.1 million a year and wiping out part of the savings before the settlement even takes effect.

“The settlement gives Visa and Mastercard the ability to increase their own fees as much as they want at any time,” Jeon said. “The settlement and its many loopholes do not help solve any of the central problems with credit card swipe fees.”

Visa and Mastercard each centrally set the swipe fee rates charged by all banks that issue credit cards under their brands and also block transactions from being processed over competing networks that offer lower fees and better security.

The CCCA would ensure that cards from the nation’s largest banks be able to be routed over at least one competing network like NYCE, Star, Shazam or Discover in addition to Visa or Mastercard’s networks. Banks would choose which networks to enable but merchants would then choose which to use, meaning networks would have to compete over fees, security and service, saving merchants and their customers an estimated $15 billion a year. Financial institutions with less than $100 billion in assets – including all community banks and all but one credit union – would be exempt.

About MPC

The Merchants Payments Coalition represents retailers, supermarkets, convenience stores, gasoline stations, online merchants and others fighting for a more competitive and transparent card system that is fair to consumers and merchants. Follow MPC on Twitter, Facebook or LinkedIn for the latest on swipe fees.